Property foreclosures are on the rise across the U.S., amid growing costs of homeownership and a wider deterioration of Americans’ financial outlook.

According to property data firm Attom, cited by CBS News, the total number of foreclosure filings reached 35,697 in August, and these have risen for six straight months year-over-year in 2025. Realtor.com, in a recent analysis, found that foreclosure rates are now up nearly 20 percent compared to the same time last year.

Why It Matters

While Attom CEO Rob Barber said that these figures remain “within a historically reasonable range,” he noted that the this trend could be “an early indicator of emerging borrower strain in some areas.”

The U.S. property market has been sending a number of concerning signals in 2025, with elevated mortgage rates and the high costs of upkeep weighing on many homeowners.

Persistent high prices and general financial strains have dampened buyer demand while putting pressure on sellers, and some economists have warned that weakness in the property sector could both signal and translate into a broader challenge for the U.S. economy.

What To Know

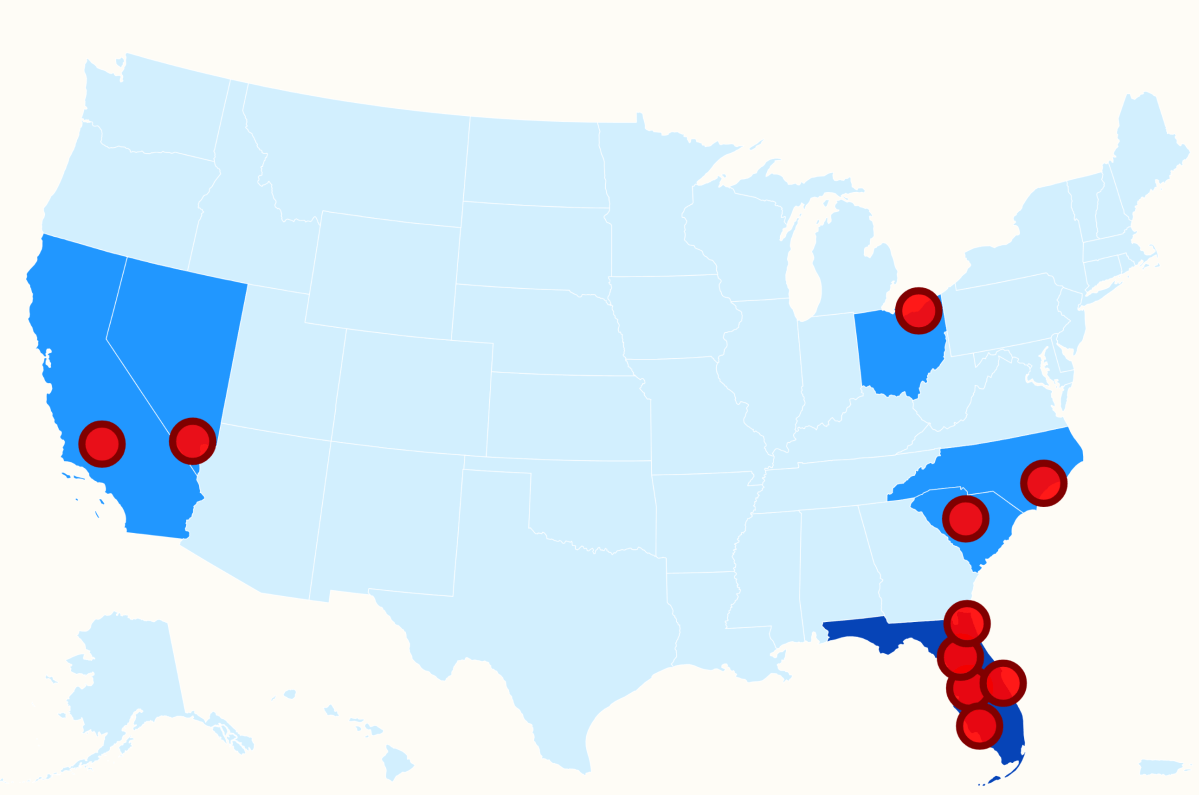

According to Realtor.com’s analysis, one in every 1,402 housing units in the U.S. had a foreclosure filing in the third quarter of this year. By reviewing foreclosure rates—the number of properties per filing—across 225 metropolitan areas with a population of at least 200,000, it identified the ten markets with the highest levels of foreclosure activity.

Lakeland, Florida was found to be the area with the worst foreclosure rate in the U.S., with one filing for every 470 housing units.

The remaining markets in Realtor’s top ten were:

- 2. Columbia, South Carolina. Foreclosure rate: 506

- 3. Cape Coral-Fort Myers, Florida. Foreclosure rate : 589

- 4. Cleveland, Ohio. Foreclosure rate: 593

- 5. Ocala, Florida. Foreclosure rate: 665

- 6/7. Jacksonville, Florida. Foreclosure rate: 673

- 6/7. Palm Bay, Florida. Foreclosure rate: 673

- 8. Bakersfield, California. Foreclosure rate: 675

- 9. Las Vegas, Nevada. Foreclosure rate: 696

- 10. Jacksonville, North Carolina. Foreclosure rate: 699

As Realtor.com noted, “it’s no coincidence that three of the top five markets are in the Sunshine State.”

Florida has been at the center of America’s new housing crisis, marked by sluggish demand, declining home valuations, and a growing disparity between renting and buying costs that have prompted some to warn that a “bubble” is forming in key markets like Miami.

Reator.com analysts attributed the state’s high foreclosure rates to a mix of rising insurance premiums, homeowners association (HOA) fees, as well as weakening buyer demand that is troubling sellers and seeing many owners lose equity.

What People Are Saying

Geoff Smith, executive director of the Institute for Housing Studies at DePaul University, told CBS News that insurance costs, interest rates and property taxes have placed “increasing pressure on existing homeowners to continue to be able to afford and pay for their mortgages.”

Hannah Jones, senior economic research analyst at Realtor.com, said: “Foreclosure rates in Florida may be relatively high due to some combination of surging insurance premiums, climbing HOA fees, and falling buyer demand.”

“Additionally, many homeowners who were protected by pandemic-era forbearance or relief programs are now facing resumed payments they can’t afford in light of rising HOA and insurance costs,” she added.

What Happens Next

There have been some encouraging developments for the housing market, with mortgage rates—considered a key linchpin—now easing. But, these may take some time to work through to the everyday economy, and so giving people slightly lower monthly payments and easing financial pressures.

Read the full article here